Navigating FEOC: Understanding the Impacts on Solar Projects

Safe Harbor remains a powerful strategy for securing tax benefits. This whitepaper with Cherry Bekaert explains new IRS guidance, FEOC considerations, timeline relief, and how to preserve full project value.

The renewable energy landscape has entered a new phase of complexity. With the expansion of Foreign Entity of Concern (FEOC) rules and new IRS guidance issued in early 2026, investors and project stakeholders must now navigate a more detailed compliance framework when pursuing solar tax credit strategies.

For impact investors and capital partners, the stakes are significant. Proper structuring and timing of solar investments may determine whether projects qualify for federal tax credits at all. At the same time, recent guidance has provided welcome clarity and workable pathways forward for compliant projects.

Brightwell’s newly released FEOC analysis outlines what has changed, what remains uncertain, and where opportunities still exist for investors and project partners. This article highlights key insights from that analysis and explains why understanding FEOC compliance has become essential for anyone involved in solar tax credit planning.

If you are evaluating solar investments or planning projects in 2026 and beyond, now is the time to understand the evolving rules.

Background

The enactment of the One Big Beautiful Bill Act (OBBBA) in July 2025 significantly expanded FEOC restrictions across the renewable energy industry. These provisions were designed to prevent certain entities connected to China, Russia, Iran, or North Korea from benefiting from U.S. renewable energy tax credits.

Prior to this legislation, FEOC provisions had limited relevance for solar tax credits. That changed quickly as policymakers expanded the rules to include both ownership/control considerations and equipment sourcing. The result is a more comprehensive compliance framework that affects how projects are structured, financed, and executed.

In February 2026, IRS Notice 2026-15 provided the first meaningful implementation guidance for these expanded rules. While not final regulations, the notice offers interim direction that investors and developers may rely on for projects beginning construction after December 31, 2025.

The new framework reflects broader policy goals: strengthening domestic supply chains, limiting reliance on certain foreign entities, and ensuring U.S. tax incentives align with national economic priorities. For investors and nonprofits alike, it introduces both complexity and opportunity.

Core Framework: How FEOC Compliance Works

At its core, FEOC compliance now hinges on two major considerations:

1. Ownership, Control, and Influence

Solar tax credits may be denied if a project owner or related entity is classified as a Prohibited Foreign Entity (PFE). A PFE includes entities tied to certain foreign governments or companies through ownership, governance rights, contractual influence, or technology licensing arrangements.

Two subcategories are particularly important:

- Specified Foreign Entity (SFE): Entities with significant ownership ties to designated countries.

- Foreign-Influenced Entity (FIE): Entities where foreign counterparties have board, debt, or contractual influence sufficient to exert “effective control.”

If a project is deemed to be controlled or influenced by such an entity, tax credits may be disallowed entirely. In some cases, previously claimed credits could be subject to recapture if non-compliant arrangements emerge after project completion.

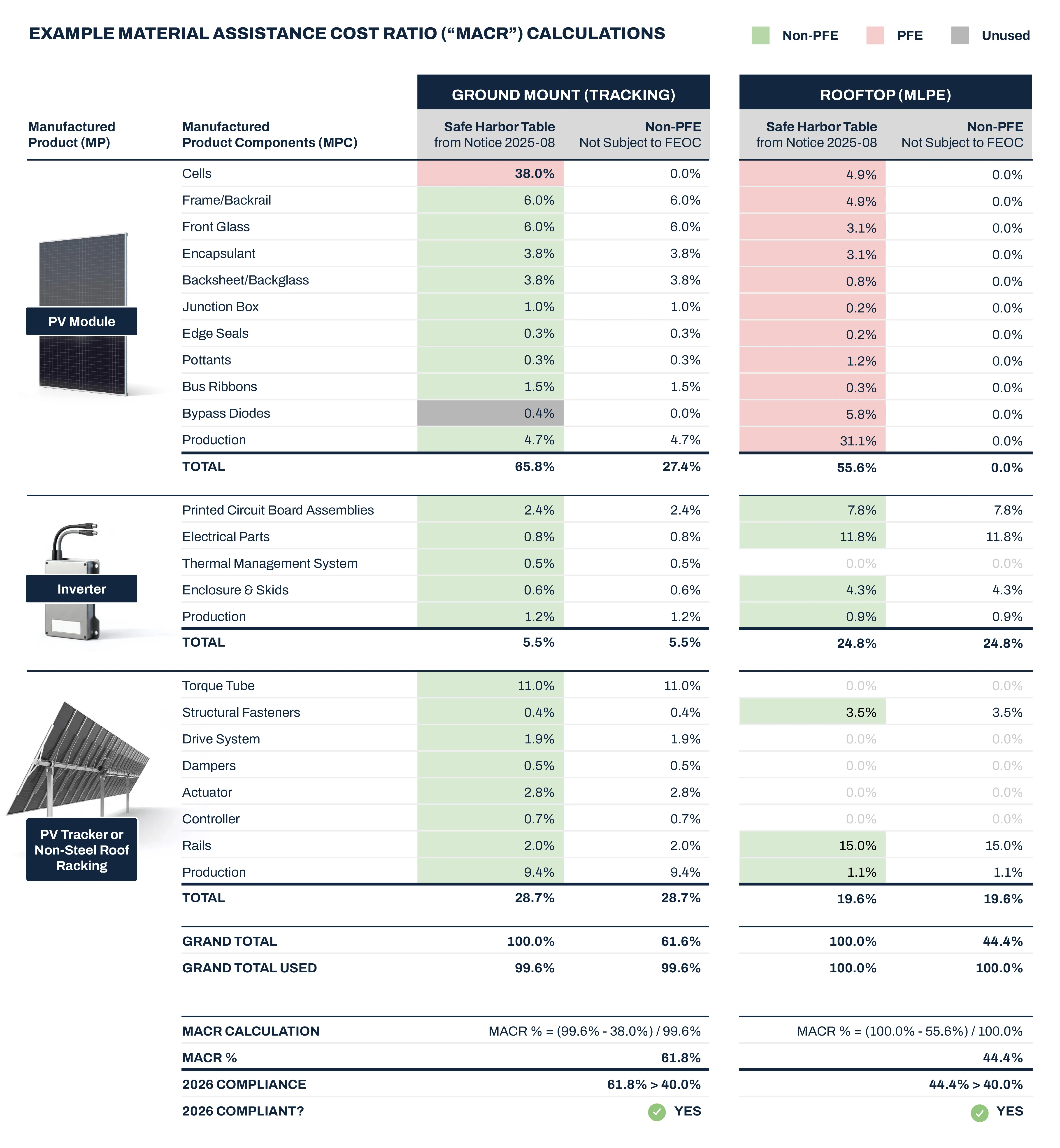

2. Material Assistance Cost Ratio (MACR)

In addition to ownership considerations, projects must evaluate equipment sourcing through the Material Assistance Cost Ratio (MACR). This calculation determines how much project equipment originates from non-prohibited sources.

For solar projects beginning construction in 2026, the applicable MACR threshold is 40%, increasing by 5% annually until reaching 60%.

To simplify compliance, IRS guidance introduced three key safe harbors:

- Identification Safe Harbor: Allows use of established domestic content tables to define relevant components.

- Cost Percentage Safe Harbor: Permits reliance on predefined cost percentages rather than tracking actual costs.

- Certification Safe Harbor: Enables reliance on supplier certifications confirming equipment sourcing.

Together, these safe harbors provide a practical pathway for demonstrating compliance when properly documented.

Market and Timing Implications

The timing of these rules is critical. Projects that began construction before January 1, 2026 are generally not subject to MACR requirements. Projects beginning in 2026 and beyond must comply with the new thresholds and documentation standards.

This creates a defined transition period across the industry. Investors and developers must now evaluate:

- Equipment sourcing and supplier certifications

- Ownership and contractual structures

- Safe harbor eligibility and construction timing

- Long-term compliance over the life of the tax credit

Importantly, IRS Notice 2026-15 is considered interim guidance. Treasury and the IRS have indicated that additional proposed and final regulations are forthcoming, particularly related to ownership and foreign-influence interpretations.

This evolving regulatory environment means decisions made today should account for future clarification and potential adjustments.

Brightwell’s Perspective

At Brightwell, FEOC guidance is viewed not simply as a regulatory hurdle but as a framework that can be navigated with the right expertise and planning.

The current guidance suggests that compliance is achievable when projects are structured intentionally and documented carefully. Safe harbor tables, supplier certifications, and clear ownership structures provide workable pathways for qualifying projects.

Brightwell’s integrated approach combines financial structuring, tax planning, engineering, and project management to help investors and nonprofit organizations navigate these requirements with confidence. The goal is to transform complex tax policy into actionable, compliant opportunities that support long-term community impact.

For investors, this means evaluating projects through both a financial and regulatory lens. For nonprofits and project sponsors, it means engaging partners who understand the full scope of compliance obligations.

Next Steps for Readers

Understanding FEOC requirements is now essential for anyone considering solar tax credit strategies in 2026 and beyond. While recent guidance has clarified several key areas, the details matter. Compliance hinges on careful structuring, documentation, and timing.

To explore the full analysis, definitions, safe harbor strategies, and example calculations, download Brightwell’s complete FEOC whitepaper:

The full publication provides detailed explanations, illustrative calculations, and frequently asked questions designed to help investors and stakeholders make informed decisions.

As with any tax-related strategy, readers should consult qualified advisors familiar with their specific circumstances before taking action.

FAQ

What is FEOC and why does it matter for solar investors?

FEOC rules determine whether certain foreign-linked entities can benefit from U.S. renewable energy tax credits. Non-compliance may disqualify projects from claiming credits entirely.

When do the new material assistance rules apply?

MACR-related rules generally apply to projects beginning construction after December 31, 2025, based on current IRS guidance.

Can projects still qualify for solar tax credits under FEOC rules?

Yes. Current guidance provides safe harbors and thresholds that many projects may meet when properly structured and documented.

Will additional guidance be released?

Yes. IRS Notice 2026-15 is interim guidance. Treasury and the IRS have indicated that additional proposed and final regulations are expected.

Where can I review the full analysis?

The complete Brightwell FEOC whitepaper includes detailed calculations, definitions, and compliance considerations. Download it using the link above.

Perspectives on modern operations and smart growth.

Let’s chat to see how we can unlock new opportunities for impact, together.